Global supply chain pressures climbed to their highest level since the pandemic-era disruptions of late 2022 in April 2026, as manufacturers accelerated safety stockpiling in response to inflation concerns, shortages and disruption linked to the war in the Middle East.

- GEP Index Signals Renewed Supply Chain Strain Across Global Manufacturing Networks

- April 2026 Regional Key Findings

- April 2026 Key Findings

- Manufacturers Increase Inventory Buffers as Shortages Intensify

- Transportation Costs Reach Record High

- GEP Warns Supply Chain Normalisation Could Take Up to 12 Months

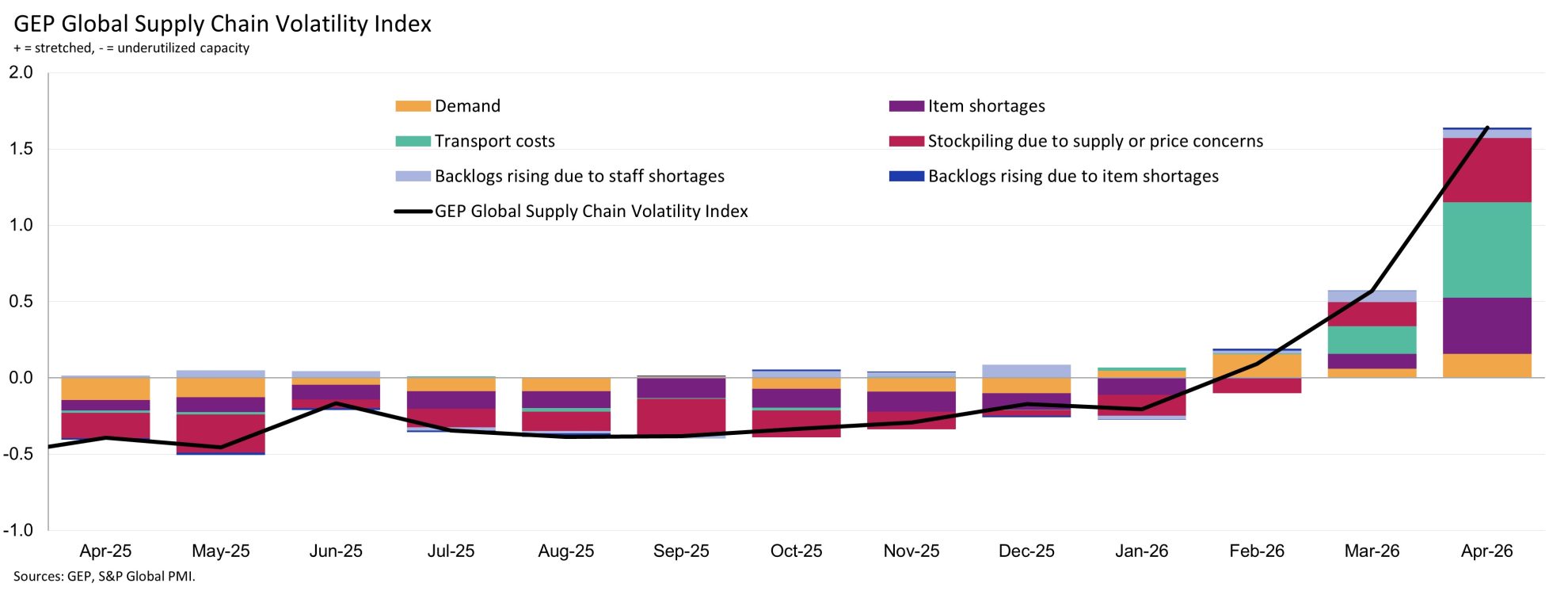

- What is the GEP Global Supply Chain Volatility Index?

GEP Index Signals Renewed Supply Chain Strain Across Global Manufacturing Networks

According to the latest GEP Global Supply Chain Volatility Index, produced by GEP and S&P Global, the index rose to 1.64 in April from 0.57 in March, marking its highest reading since October 2022.

The index, based on monthly survey data from around 27,000 businesses across more than 40 countries, showed manufacturers increasing purchasing activity and building inventory buffers to secure supply ahead of further price rises and supply disruption.

April 2026 Regional Key Findings

- ASIA: Index soars to 3.79, from 1.16, its highest in more than four years. Surging transportation costs were a key factor behind the index’s increase, with the region more reliant on Middle East oil than other parts of the globe.

- NORTH AMERICA: Index jumps to 1.52, from 0.42, a 44-month record. Manufacturers in the U.S. and Canada purchased more materials to build inventories, leading to a sharp squeeze on supply chain capacity in the continent.

- EUROPE: Index rises to 1.64, from 0.64, a three-and-a-half-year high, as European manufacturers safety stockpiled more than any other part of the globe.

- U.K.: Index rises to 0.96, from 0.16, its highest reading since December 2022.

April 2026 Key Findings

- DEMAND: Global demand for production inputs such as raw materials, commodities and intermediate goods rose in April, with purchasing its strongest in more than four years. The expansion reflected front-loaded buying activity in anticipation of price inflation and supply disruption, rather than growth due to improving underlying manufacturing conditions.

- INVENTORIES: To mitigate further price rises and supply disruption, global manufacturers built buffers into their inventories more aggressively. Reports of safety stockpiling surged higher in April and were their most widespread since January 2023 as oil prices remained volatile and uncertainty regarding the war in the Middle East continued.

- MATERIAL SHORTAGES: The items in short supply indicator rose again in April to its highest in nearly three-and-a-half years, signaling that shortages of critical materials and inputs were the highest since late 2022, towards the end of the post-pandemic supply squeeze.

- LABOR SHORTAGES: Labor shortages remained contained in April, although they were marginally above the long-run average at the global level. By region, reports of manufacturing backlogs rising due to staff shortages were their greatest in Europe.

- TRANSPORTATION: The global transportation costs tracker soared to a record high in April (data were first collected in 2005), reflecting surging fuel prices, as well as rising maritime shipping and freight rates.

Manufacturers Increase Inventory Buffers as Shortages Intensify

The report found that global manufacturers ramped up safety stockpiling of goods and raw materials at the fastest rate in three years.

European manufacturers reported the most aggressive inventory building activity, while purchasing activity globally reached its strongest level in more than four years.

At the same time, reports of item shortages rose to their highest level since November 2022, signalling renewed pressure on suppliers and logistics networks.

According to the report, the increase in purchasing activity reflected front-loaded buying in anticipation of further disruption and inflation, rather than underlying improvements in manufacturing demand.

Transportation Costs Reach Record High

Global transportation costs climbed to a record high in April, according to the index data, driven by maritime disruption, rising freight rates and higher fuel prices linked to geopolitical tensions in the Middle East.

Asia recorded the sharpest deterioration in supply chain conditions, with the regional index surging to 3.79 from 1.16, its highest level in more than four years.

North America’s index rose to 1.52 from 0.42, while Europe’s increased to 1.64 from 0.64, both reaching multi-year highs as manufacturers increased inventory purchases and safety stock levels.

The UK index also climbed sharply to 0.96 from 0.16, its highest reading since December 2022.

GEP Warns Supply Chain Normalisation Could Take Up to 12 Months

“Even if tensions in the Middle East ease quickly, global supply chains are unlikely to normalize for another six to 12 months,” said John Piatek, vice president, consulting, GEP.

“What stands out in April’s data is how broadly the disruption is spreading. Shortages worsened across every major region, signaling this is no longer an isolated transport shock. Companies worldwide are now scrambling to secure supply and protect themselves against further inflation and disruption.”

The report also noted that labour shortages remained relatively contained globally in April, although European manufacturers reported the greatest increase in backlogs linked to staffing constraints.

What is the GEP Global Supply Chain Volatility Index?

The GEP Global Supply Chain Volatility Index is produced by GEP and S&P Global using data derived from S&P Global PMI surveys covering around 27,000 companies in more than 40 countries.

The index measures global supply chain stress using six sub-indices based on purchasing activity, inventory trends, shortages, transportation costs and labour constraints.

A reading above zero indicates supply chain capacity is being stretched and volatility is increasing, while a reading below zero signals underutilised capacity and easing supply chain pressures.

Regional indices are also published for Asia, Europe, North America and the UK.

This article was produced by the editorial team at Supply Chain Outlook and published as part of the Outlook Publishing global network of B2B industry magazines.

Outlook Publishing delivers industry insights, company stories, and sector coverage across supply chains, manufacturing, mining, construction, healthcare, food production, and sustainability.

Supply Chain Outlook provides ongoing coverage of organisations and developments shaping the global logistics and supply chain sector.